W-2 Filing Checklist - Helpful Tips for Preparing 2012 W-2’s (Part I)

The holidays, year-end and tax filing deadlines can make this a stressful time of year. We hope you find the information helpful while preparing...

3 min read

The holidays, year-end and tax filing deadlines can make this a stressful time of year. We hope you find the information helpful while preparing...

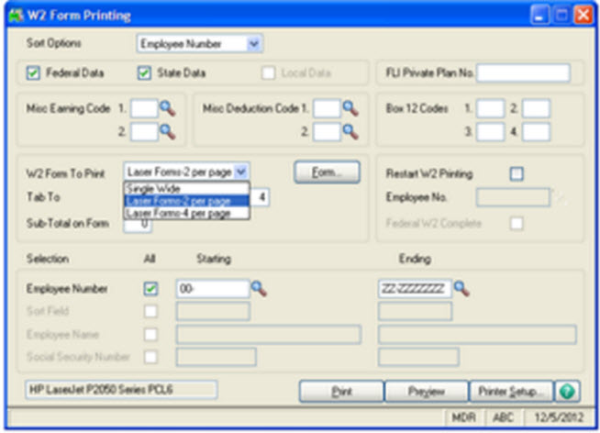

Question: Mike, we own Sage 100 ERP (formally Sage MAS90), we process Payroll. How do we run the year end W2 forms.

Sage 100 Consultant Tip: What to do when Paperless Office won't print Sage 100 ERP consultant, we had a client who had a technical issue with...